The Development of Islamic Finance in the USA: Investing Options for 2026

How Shariah-compliant financial services evolved from niche offerings to mainstream investment solutions

January 28, 2026

1-Min Summary

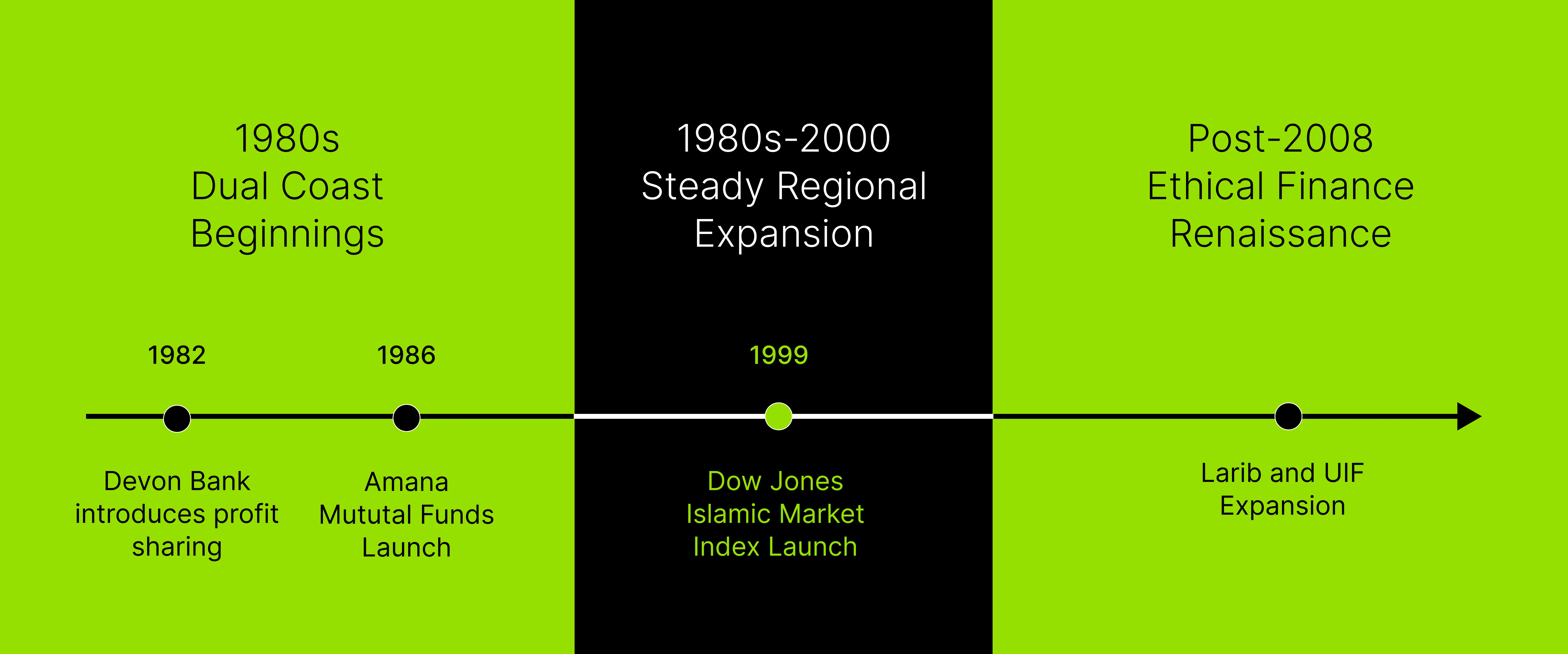

Origins & Growth — Islamic finance in the US started in the early 1980s with community-level banking and has grown into a ~$250 billion market with 43 institutions offering Shariah-compliant products.

Key Products — Investors can access halal ETFs (SPUS, HLAL), 7 mutual funds managing $3.6B (led by Amana), sukuk bonds, and Islamic home financing through providers like UIF and LARIBA.

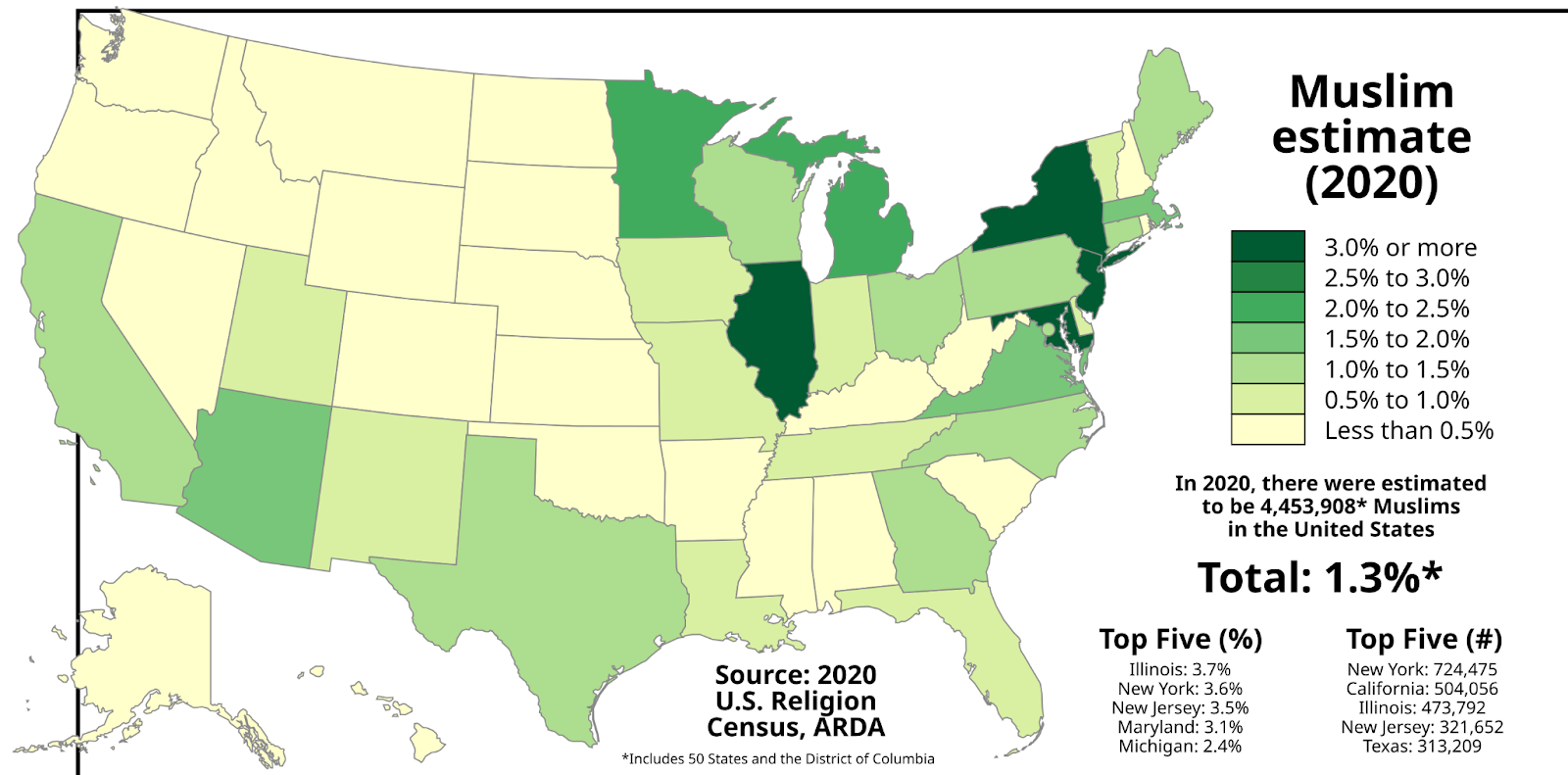

Demographics Driving Demand — American Muslims hold an estimated $170B in purchasing power, skew younger than the national average, and are concentrated in metro areas like NYC, LA, Chicago, and Detroit.

Challenges Remain — The sector still faces limited product variety (7 Islamic funds vs. 7,000+ conventional), higher expense ratios, low awareness (78% of US Muslims unaware of options), and minimal 401(k) availability.

Future Outlook — Projected to reach $400B by 2030, driven by fintech innovation (robo-advisors, AI screening), ESG convergence attracting non-Muslim investors, and improving regulatory frameworks.

Updates Log

Feb 1, 2025

From Coast to Coast: Islamic Finance Growth Timeline

Islamic finance in America began with geographically dispersed initiatives serving immigrant communities seeking banking alternatives that matched their religious beliefs. Today, it represents a significant segment of the global financial system.

Current Market Size and Demographics

Verified Market Data

US Islamic Finance Assets:

$3.6 billion in Islamic mutual funds (7 funds total)

$1.1 billion raised through Sukuk issuances (5 issuers)

$250 billion estimated total US Islamic finance market size

Amana Growth Fund (AMAGX): $1.2 billion assets, 1.04% expense ratio

Amana Income Fund (AMANX): $800 million assets, 0.88% expense ratio

Amana Developing World Fund (AMDWX): $400 million assets

Other Providers:

Azzad Ethical Fund (ADJEX): $300 million assets, 1.25% expense ratio

Iman Fund (IMANX): Capital appreciation focus, 1.20% expense ratio

Sukuk Market Development

Current Landscape:

5 active Sukuk issuers in the US market

$1.1 billion total raised cumulatively

AAOIFI Standard 62: New proposed regulation requiring actual asset ownership transfer to investors

2025 Sukuk Developments: The proposed AAOIFI Standard No. 62 aims to strengthen Shariah compliance by ensuring genuine asset ownership transfer to investors. This development may increase issuance costs and complexity but reinforces authentic Islamic finance principles.

Available Sukuk Types:

Corporate sukuk from major corporations

Real estate-backed sukuk

Infrastructure project financing

Yields typically ranging 2-5% based on duration and credit quality

Islamic Home Financing

University Islamic Financial (UIF) Leadership: UIF Corporation provides comprehensive Islamic home financing through:

Murabaha Model: Cost-plus financing structure

Ijarah Model: Lease-to-own arrangements

Geographic Coverage: Multiple states nationwide

Product Range: Home, car, and commercial real estate financing

Regulatory Framework and Compliance

Federal Recognition and Accommodation

Securities and Exchange Commission (SEC): Islamic investment advisors must register as Registered Investment Advisors (RIAs), providing the same consumer protections as conventional advisors while accommodating Shariah requirements.

Court Recognition: US courts increasingly acknowledge Islamic contracts and financing structures, providing legal legitimacy to Islamic finance transactions.

AAOIFI Standards Evolution

Standard 62 Development: AAOIFI's proposed Standard No. 62 for Sukuk represents significant regulatory advancement:

Objective: Ensure actual asset ownership transfer to investors

Impact: Strengthen Shariah authenticity of Sukuk structures

Challenges: May increase issuance costs and structural complexity

Timeline: Expected implementation throughout 2025

Existing Framework:

Business activity screening (prohibited industries)

Financial ratio thresholds (debt, cash, receivables limits)

Income purification requirements

Independent Shariah board oversight

Challenges and Market Barriers

Scale and Product Limitations

Limited Universe:

7 Islamic mutual funds vs. 7,000+ conventional mutual funds

4 major Shariah ETFs vs. 2,000+ conventional ETFs

Higher expense ratios due to specialized screening and smaller scale

Mobile Apps: Real-time screening and compliance monitoring

Digital Platforms: Streamlined account opening and management

ESG Convergence

Ethical Investing Alignment: Islamic finance principles align with Environmental, Social, and Governance (ESG) criteria:

Environmental: Exclusion of harmful industries

Social: Emphasis on ethical business practices

Governance: Transparency and stakeholder considerations

Market Opportunity: ESG investing attracts non-Muslim investors to Islamic finance products, expanding the addressable market beyond the Muslim community.

Blockchain applications for transparent Sukuk trading

Digital-first Islamic financial institutions

The Bottom Line

Islamic finance in America has matured from experimental community initiatives to a $250 billion market serving diverse investment needs. With 43 institutions now offering Shariah-compliant products and 7 mutual funds managing $3.6 billion, the infrastructure supports both religious requirements and competitive investment returns.

Market Reality Check: The US Islamic finance sector remains smaller than conventional alternatives, with higher fees and fewer product choices. However, the 8-12% annual growth rate and expanding demographic base indicate substantial future potential.

Key Success Factors:

Product diversification beyond current limited offerings

2026 Outlook: Expect continued growth driven by demographic trends, ESG investment convergence, and technological innovation. The sector's evolution from niche community service to mainstream financial alternative positions it for significant expansion over the next decade.

For investors considering Islamic finance options, the current landscape offers viable alternatives to conventional investing while maintaining Shariah compliance. The combination of established institutions, emerging technology platforms, and improving regulatory framework creates a foundation for sustained growth and product innovation.

To get a free consulting call from NoorVest, Get Started: